Hotel performance found some normalcy this past week after an underwhelming start to March. A combination of Group, Business, and Leisure travel helped stabilize the market, bringing us back into the range of “normal” market dynamics for this time of year. Pt. Loma, UTC, and I-15 Corridor properties continued to see brisk midweek demand, a telltale sign that business meetings are still alive and well in the region for the time being, while Downtown, Mission Valley, Mission Bay each saw occupancy above 90% on Saturday night, indicating a boost from the leisure segment. Mission Bay saw sustained occupancy above 70% for the entire week.

Here are the details:

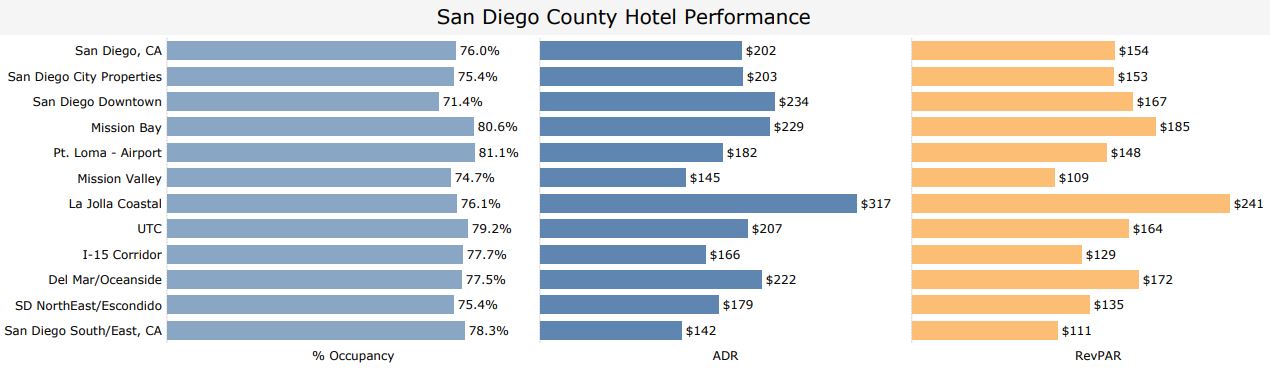

- San Diego hotels sold 344,713 room nights last week, matching room demand in 2023 and 2024.

- Occupancy averaged 76.0%, a 0.6% YoY increase. Even so,San Diego barely cracked the top 10 among the 25 largest markets tracked by STR and 5th in the western comp set behind Phoenix (85.1%), Orange County (83.8%), San Francisco (77.5%), and Los Angeles (77.5%).

- The top 3 markets last week were New York (86.1%), Miami (86.0%), and Tampa (85.9%).

- The top 3 submarkets last week were Pt. Loma (81.1%), Mission Bay (80.6%), and UTC (79.2%).

- ADR was $202, a 0.6% YoY increase.

- Upscale+ properties sold 51,670 GROUP room nights, on par with last year, with an ADR of $291 (-0.1% YoY).

View the complete hotel performance report here.

Leave a Reply