- San Diego County hotel demand softened from the previous week to sell a total of 343,338 room nights last week. This is roughly 16,500 fewer room nights than were sold the same week in 2019, owing entirely to a drawdown in leisure demand. The leisure segment is showing signs of fatigue as consumers continue to grapple with decades-high inflation, stock price declines and volatility, and the threat of a looming recession.

- ADR is also cooling and coming closer to past years’ levels. Last week’s average of $213 is $15 higher than the same week in 2021 and nearly $40 higher than 2019, but the gap has been narrowing in recent weeks, in line with forecasts showing a reduction in ADR as we head into 2023.

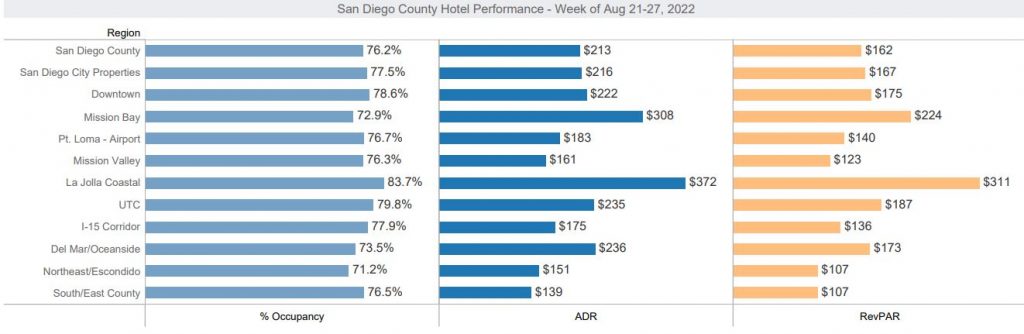

- County occupancy dipped slightly from the previous week to land at 76.2% but San Diego maintains its position in the top 5 markets nationally. The top three markets last week were Oahu Island (81.9%), Boston (81.5%) and New York (78.0%).

- La Jolla Coastal properties had the highest average occupancy for the week at 83.7%, followed by UTC at 79.8%.

- RevPAR followed suit, falling $15 week-over-week to settle at $162 last week.

- The convention center hosted SPIE from August 23-25 for a total of 5,500 blocked room nights. Group occupancy among upscale+ properties averaged 22.8%, peaking on Tuesday at 30.2%. In total, Group demand was 42,489 RNs with an ADR of $252, roughly 1,500 fewer RNs than the same week in 2019 but collecting a $7 higher rate.

- Transient demand also mirrored that of the same week in 2019 with 93,416 total RNs sold last week. Similar to the broader market, Transient ADR continues to outperform past years by an average of $65 per night.

Leave a Reply