San Diego County hotel performance remains volatile. Demand cooled last week following a boost from the WWE Survivor Series over Thanksgiving weekend. The absence of ASH this year also played a significant role in softening demand for the weeks of November 30 and December 7.

More broadly, demand has been uneven throughout much of 2025, ASH notwithstanding.

Recently, hotels have begun sacrificing rate to protect occupancy—a trend that started in late September. Since then, demand is down 0.9% year-over-year—not ideal, but not alarming. However, ADR has fallen 3.9% compared to the same period last year. Combined, hotel revenues from September 21 through December 13 are down 4.8%.

This past week alone, ADR slipped from 7th place among the top 25 markets last year to 10th place in 2025.

On a positive note, room nights currently on the books (OTB) for the first four months of 2026 look stronger than they did this year, according to TravelClick data.

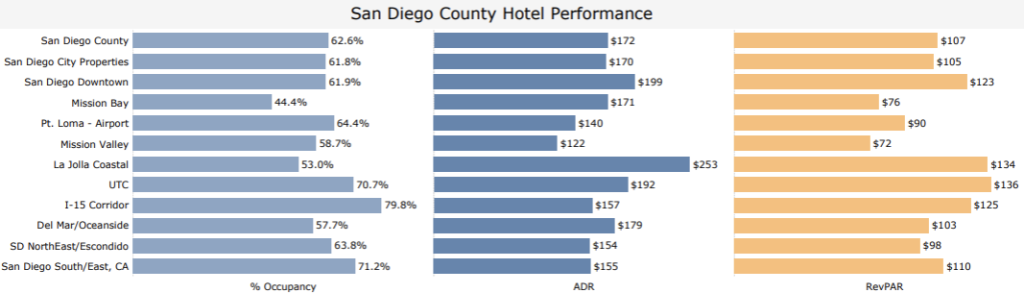

Weekly Hotel Performance: December 7-13, 2025

· Room Demand: 293,157 room nights (-5.6% YoY).

· Occupancy: 62.6% (-8.3% YoY); 15th among the top 25 U.S. markets and 5th in the western competitive set, only ahead of Seattle (62.2%; -2.9% YoY).

o Top Performing US Markets: New York (92.5%; -0.8% YoY), Oahu Island (78.7%; +2.6% YoY), and Miami (77.6%; -0.2% YoY).

o Top Performing Western Competitive Markets: Orange County (77.5%; +9.2% YoY, Phoenix (73.8%; +8.9%), and Los Angeles (68.1%; +2.5% YoY).

o Top Performing Local Areas: I-15 Corridor (79.8%; +2.4% YoY), UTC (70.7%; -9.5% YoY), and Pt. Loma (64.4%; -11.5% YoY)

· ADR: $171.53 (-12.3% YoY).

· RevPAR: $107.36 (-19.5% YoY).

· Group Performance (Upscale+ Properties) and Convention Activity:

o Room Demand: 50,067 group room nights (-11.1% YoY).

o Occupancy: 24.1% (-18.1% YoY).

o ADR: $247.80 (-9.5% YoY).

o RevPAR: $59.81 (-25.8% YoY).

View the complete hotel performance report here.

Leave a Reply