Compared to last year, San Diego hotels posted softer results. Occupancy declined on weaker-than-usual seasonal demand, while average rates slipped below 2024 levels, reflecting reduced pricing power and limited compression tied to a sharp drop in Group room nights. Coastal and downtown properties continued to lead on rate, but overall growth stalled.

With half of November complete, trends remain weak relative to 2024. Demand is down 3.0% year over year, while supply is up 3.5%, driving a 6.3% decline in occupancy for the month-to-date. Coupled with a 3.7% drop in ADR, RevPAR is tracking at -9.7% versus the first half of November last year.

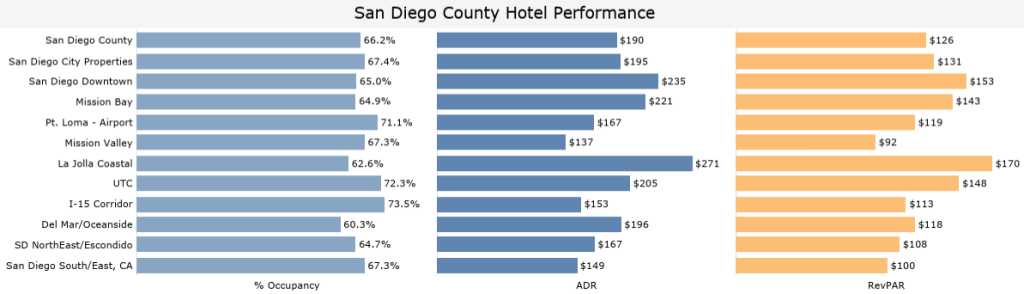

Weekly Hotel Performance: November 9-15, 2025

• Room Demand: 311,041 room nights (-9.7% YoY).

• Occupancy: 66.2% (-12.7% YoY); 13th among the top 25 U.S. markets and 4th in the western competitive set.

- Top Performing US Markets: New York (88.7%; -1.5% YoY), Miami (78%; -5.3% YoY), and Phoenix (77.9%; -2% YoY).

- Top Performing Western Competitive Markets: Phoenix, Orange County (73.7%; +4.0% YoY), and Los Angeles (70.8%; -6.2% YoY).

- Highest Performing Areas Locally: I-15 Corridor (73.5%; +2.0% YoY), UTC (72.3%; -14.2% YoY), and Pt. Loma-Airport (71.1%; -11.0% YoY).

• ADR: $190.43 (-8.1% YoY).

• RevPAR: $125.99 (-19.7% YoY).

• Group Performance (Upscale+ Properties) and Convention Activity:

- Room Demand: 61,165 group room nights (-19.6% YoY).

- Occupancy: 29.3% (-26.7% YoY).

- ADR: $280.78 (-3.4% YoY).

- RevPAR: $82.17 (-29.1% YoY).

- Convention Center Activity: Last week, the convention center hosted the Athletic Business Show and the 2025 Annual Society for Neuroscience, generating a combined total of 13,886 room nights to the market.

- Last year, there were two mid- to large-sized events that were not in town this year—the International Foundation of Employee Benefit Plans (~22,500 RNs) and the American Association for the Study of Liver Disease (~9,700 RNs)

View the complete hotel performance report here.

Leave a Reply