After a strong start to the year in January, San Diego’s hotel market has begun to feel softer. Whether or not this is directly related to policy uncertainty emanating from Washington remains to be seen, but nascent reports of group cancellations tied to government policies have begun to surface. We will continue to monitor these trends closely and update you as more data and information is available.

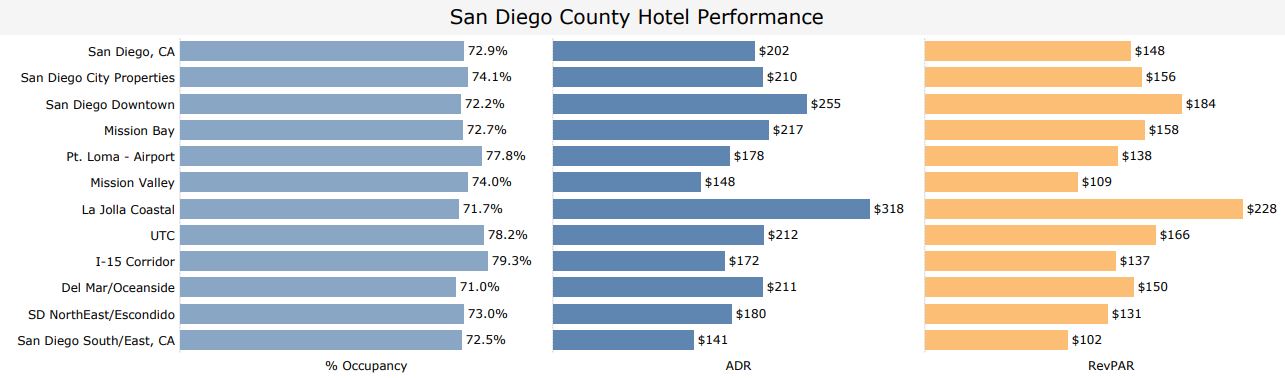

Overall Market Performance:

- Occupancy Rate: 72.9%, a 4% YoY decrease.

- National Ranking: 7th among the Top 25 U.S. Markets.

- Western Competitive Set: 3rd place.

- Average Daily Rate (ADR): $202.49.

- Revenue per Available Room (RevPAR): $148.

- Room Nights Sold: 330,477, a slight decrease of 13,300 compared to the same week in 2024.

Top-Performing Submarkets:

- I-15 Corridor: 79.3% occupancy.

- UTC: 78.2% occupancy.

- Point Loma-Airport: 77.8% occupancy.

- The above areas experienced mid-week occupancy spikes, indicating solid business travel activity.

Competitive Market Analysis:

- Leading U.S. Markets:

- Miami: 88.9% occupancy, driven by major events such as the Montreux Jazz Festival, South Beach Wine & Food Festival, and the Miami Open.

- Oahu Island: 85% occupancy.

- Phoenix: 84.7% occupancy, bolstered by events like The Phoenix Travel & Adventure Show and the Scottsdale Arabian Horse Show.

Upscale+ Segment Performance:

- Occupancy Rate: 34%, a 3.5% year-over-year increase.

- ADR: $306.94.

- RevPAR: $104.

- Room Nights Sold: 67,232, an increase of 7,300 compared to the same week last year.

Group and Convention Activity:

- San Diego Convention Center Events: Three significant events contributed a total of 24,354 group room nights.

- Non-SDCC Groups: Added 7,543 room nights.

View the complete hotel performance report here.

Leave a Reply